Case Study

ChileAtiende – a multi-channel one-stop shop for public services

26th February, 2016

The initiative

In 1994, the European Commission (EC) set up the EIF to promote "the creation and development of SMEs by guaranteeing loans to SMEs and financing the venture capital funds that invest in them".[2] The EIF has two main statutory objectives:

Six years later it was brought within the ambit of the European Investment Bank (EIB). "Following the conclusion of the Lisbon European Council in March 2000, which called for increased support to assist SMEs, it was decided that the EIF should work more closely with the EIB. The EIB Group was established and the EIF became the EIB group's venture capital financing arm.”[4] The EIB owns 62% of the EIF; the other main shareholder is the EC, which holds 29% of the shares on behalf of the [5]

Since then, the EIF has evolved to meet the challenges of the twenty-first century, as shown in the following chronology:

The challenge

Throughout the EU, the majority of businesses are small and medium sized enterprises (SMEs). "SMEs represent 99% of all businesses in the EU, and employ approximately 65 million people."[1] They are essential to the economy and some go on to be large companies employing thousands of staff, but in their early stages they are often starved of finance. The problem for the EU in the 1990s was how to facilitate the SMEs' access to capital and to promote economic growth.The public impact

In 1997, the EIF began to manage its first venture capital operation, a “programme on behalf of the EIB, the European Technology Facility (ETF), a EUR125 million facility”.[7] By 2014 it had made a very considerable impact on the European economy. “It is estimated that the investment activity backed by the EIF represented 41% of total investments in Europe in 2014 (29% in 2007). The share directly attributable to the EIF amounts to 10% (5% in 2007), hinting at the significant leverage that characterises EIF-backed investments.”[8]

Its impact in the UK was typical of its investment throughout the EU. “Between 2011 and 2015, the EIF committed EUR2.3 billion to some 144 UK-based venture capital firms. That amounts to about 37% of all venture capital funding raised in the UK during those years, according to data from Invest Europe, the trade association for European Venture Capital firms.”[9]

Stakeholder engagement

The main stakeholders of the fund at the international level are the EIB and the EU, represented by the EC (see The initiative above). Financial institutions from EU member states and Turkey together hold 9% of the fund's shares between them and are important stakeholders as well as shareholders. “All Shareholders meet once a year at the Annual General Meeting (AGM), in particular to approve EIF's Annual Report and accounts as audited by the Audit Board. Shareholders also meet for information sessions during the year.”[10] The EU member states are the main stakeholders at international level, with the SMEs within the EU that have received EIF funding being the principal beneficiaries.

The EIF aims to publicise its initatives to its stakeholders. “The EIF promotes transparency as a way to strengthen its accountability. Therefore, the EIF aims to provide stakeholders with the information they require... The EIF's stakeholder engagement follows best practice, aimed at increasing mutual understanding, addressing stakeholders' concerns and adjusting its activities accordingly, targeting a possible gap between expectations, policy and practice and achieving coherence and accountability in EIF's policies and practices.”[11]

Political commitment

There was a strong political commitment within the European Council in the early 1990s to create the EIF on behalf of the EU member states: "In December 1992, [the] European Council urged the establishment of a European Investment Fund in order to promote economic recovery in Europe”.[12]Public confidence

There is no evidence of widespread public awareness of the EIF in EU members states. However, for European venture capitalists, the EIF is a very influential institution. This is apparent in the UK as it is elsewhere in the EU:

Clarity of objectives

The main objective of the EIF - to enhance SMEs' access to finance and to promote economic recovery in Europe - was defined clearly when the EIF was constituted (see The intitiative above): “by developing and offering targeted financial products to our intermediaries, such as banks, guarantee and leasing companies, micro-credit providers and private equity funds, we enhance SMEs' access to finance".[14]

These objectives have been developed over the years since 1994. “The vision and values of the EIF remain pertinent in the context of a weak economic environment in Europe and a continued shortage of risk capital and debt finance for European SMEs. To support Europe's recovery path, this Corporate Operational Plan proposes another significant expansion of the EIF activities and impact, funded by increased capital and mandate resources and further investment in human resources, systems and processes.”[15]

Strength of evidence

There is no clear documentation of the creators of the EIF drawing on evidence from similar organisations.Feasibility

The financial feasibility of the EIF has been guaranteed since its inception by the substantial majority shareholdings of the EIB and the EC (on behalf of the EU), which together hold 91% of shares in the EIF. Its legal status was secured through its relationship with the the EIB: "the EIF was established in 1994 pursuant to the Statute of the EIB under Article 28 , which empowers the Board of Governors to 'decide to establish subsidiaries or other entities, which shall have legal personality and financial autonomy'."[16]

A ruling of the European Court of Justice (ECJ) obliged the EIB, and hence the EIF, to tighten its internal rules and procedures in order to manage the risk of fraud and corruption. “Following a ruling of the ECJ on the cooperation of the EIB with OLAF [the European Anti-fraud Office], the EIB has taken steps to adapt its internal rules and procedures to the applicable legal framework, in order to ensure optimal cooperation with OLAF in the fight against fraud and corruption. Similarly, EIF has implemented cooperation principles with OLAF and issued an EIF Anti-Fraud Policy, which is published on EIF's website.”[17]

Management

The EIF's governance structure comprises representatives from the EIB, the EC, and financial institutions from the EU member states. “The Fund is a public-private partnership with a unique shareholding structure combining public and private investors. Our shareholding structure was modified in 2000, when the EIB became the majority shareholder, resulting in the formation of the EIB Group.”[18]

The EIF therefore benefits in its management from its close ties with the EIB Group and other EU institutions.“The EIF actively promotes transparency and good governance in its transactions and generally with its counterparts. The EIF integrates its policy framework into the EIB Group policies and maintains close contacts with other EU and international institutions and bodies to monitor and exchange views on new developments in the area of transparency and disclosure with a view to continuously improving its own policies and practices.”[19]

The EIF's AAA credit rating, which was accorded in 2003 (see The initiative above), reflects its robust management structure. “A strong governance is key to EIF's success and has been noted by external credit rating agencies. Further control and evaluation is carried out by several different authorities, such as:

The EIF is, in common with the other EU institutions, subject to the oversight of an ombudsman. “The European Ombudsman has the power to conduct inquiries concerning instances of maladministration in nearly all the activities of the EU institutions or bodies, including EIF as part of the EIB Group. When citizens are not satisfied with the outcome of the internal EIF complaints investigation, they have the right to contact the European Ombudsman about alleged maladministration.”[21]

Measurement

A general metric for assessing the EIF's performance is the amount of finance its has invested in SMEs in the EU (see Public impact above). There are, however, specific bodies that examine the detail of the EIF's performance very closely. An important element of the measurement of EIF performance is the work of the Operations Evaluation (EV) team. “In line with good governance, the EIB Group (EIB and EIF) strives towards constant improvement in all aspects of performance, and our EV team forms an important part of this. EV carries out independent ex-post evaluations of EIB and EIF activities. EV work is carried out mainly at a thematic level. This can be by sector, mandate or financial product. Geographical scope is usually by region or sub-region, meaning that reports will deal with the EU or the Mediterranean [area] as whole, rather than individual nations. Temporal scope is typically 10 years, but this could be revised. More specifically to EIB and EIF operations, EV examines the management of the project cycle.”[22]

The Audit Board (see Management above) also has a significant role to play. "The EIF has an independently appointed Audit Board, whose role is to confirm that EIF's operations have been carried out in compliance with the procedures laid down in EIF Statutes and in EIF's Rules of Procedure. They also verify that the accounts give a true and fair view on EIF's assets and liabilities and the results of our operations."[23]

Alignment

The main stakeholders are aligned in their efforts to enhance European SMEs' opportunities for funding. “By developing and offering targeted financial products to our intermediaries, such as banks, guarantee and leasing companies, micro-credit providers and private equity funds, [the EIF] enhances SMEs access to finance.” [24] Its place within the EIB Group assists the EIF in this respect.

There is an ongoing relationship between the EIF and its shareholders. “EIF's shareholders are represented in the General Meeting, which is a governing and decision-making body, which, where necessary, can sanction the members of the other statutory bodies. Interaction and collaboration between the shareholders and EIF is further maintained through a range of exchanges and channels of communication, including newsletters, formal and informal meetings and workshops.”[25]

There is also a close relationship with the EC. “Cooperation with the EC is vital, particularly in terms of risk capacity and achieving policy objectives. This cooperation was further reinforced in 2014 through additional new mandates (InnovFin, COSME, Erasmus+, EaSI) entrusted to EIF by the EC, under the umbrella of a Financial and Administrative Framework Agreement (FAFA) entered into between EIF and the EC. Most recently, EIF has committed itself to the implementation of the European Fund for Strategic Investments (“EFSI”), an initiative implemented in close partnership between the EC and the EIB Group.”[26]

Bibliography

Brexit, and That Huge Investment Fund You've Never Heard Of, Jeremy Khan, 1 July 2016, Bloomberg Technology

(www.bloomberg.com/news/articles/2016-07-01/brexit-and-that-huge-eu-investment-fund-you-ve-never-heard-of)

EIF Transparency Policy, 1 February 2016, European Investment Fund

(http://www.eif.org/news_centre/publications/eif-transparency_policy_01022016.pdf)

Register of Members, 15 February 2017, European Investment Fund

(http://www.eif.org/news_centre/publications/register_shareholders.pdf)

The European Investment Fund, 2015, CIVITAS Institute for the Study of Civil Society 2015

(http://www.civitas.org.uk/content/files/BO.3.EIF_.pdf)

The European venture capital landscape: an EIF perspective Volume I: The impact of EIF on the VC ecosystem, June 2016, Working Paper 2016/34, EIF Research & Market Analysis, European Investment Fund

(http://www.eif.org/news_centre/publications/eif_wp_34.pdf)

The Governance of the European Investment Fund, European Investment Fund

(http://www.eif.org/news_centre/publications/eif_governance_en.pdf)

Who we are: Our mission, European Investment Fund

(http://www.eif.org/who_we_are/index.htm)

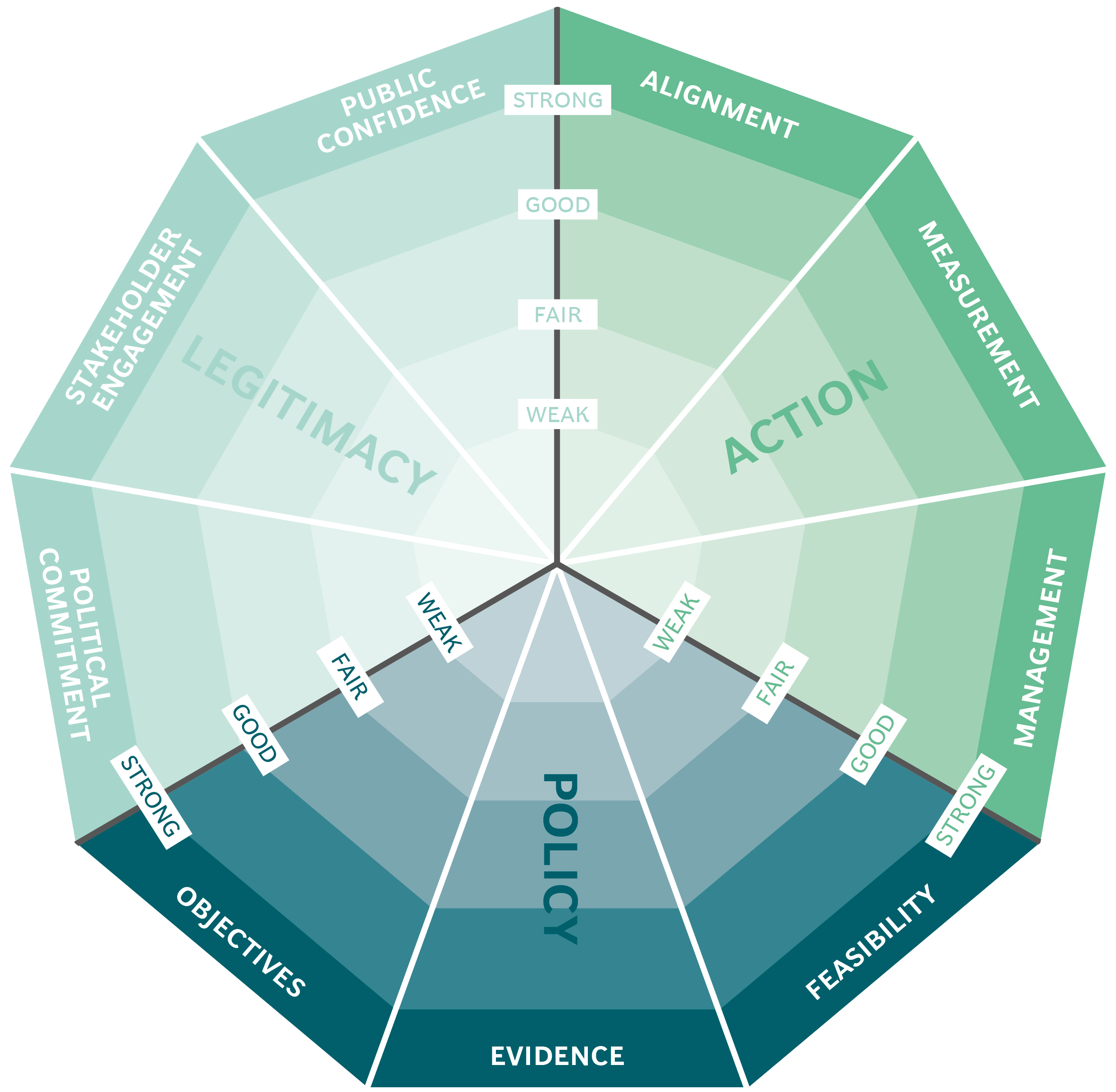

This case study has been assessed using the Public Impact Fundamentals, a simple framework and practical tool to help you assess your public policies and ensure the three fundamentals - Legitimacy, Policy and Action are embedded in them.

Learn more about the Fundamentals and how you can use them to access your own policies and initiatives.