Case Study

ChileAtiende – a multi-channel one-stop shop for public services

26th February, 2016

The initiative

In order to make formal insurance cover more widely available, the Agriculture Insurance Company of India Ltd. (AICIL) introduced a rainfall insurance scheme known as "Varsha Bima" in south west India during the 2004 monsoon period.

Varsha Bima's main aims are to:

Varsha Bima was piloted in 20 areas in the states of Andhra Pradesh, Uttar Pradesh, Karnataka and Rajasthan. [1] In Tamil Nadu, Andhra Pradesh and Uttar Pradesh states, 42 villages were randomly selected to receive a marketing visit offering a new rainfall insurance product while another 21 villages were selected to serve as a comparison group.

The challenge

Unpredictable rainfall is one of the largest sources of risk that poor Indian farming households face, because extremely low or heavy rainfall can substantially reduce crop yields and lead to big reductions in income and consumption. About 90 percent of the variation in crop production levels in India is caused by extremes in rainfall levels and patterns.

Only 10 percent of the Indian population is covered by any formal insurance against such abnormal patterns of rainfall. However, informal risk-sharing arrangements between members of the same sub-caste are common.

The public impact

During the pilot phases of Varsha Bima, researchers observed the following results regarding take-up of the insurance:

This suggests that such index insurance was able to increase average incomes by removing the barriers farmers face to planting more profitable crops.

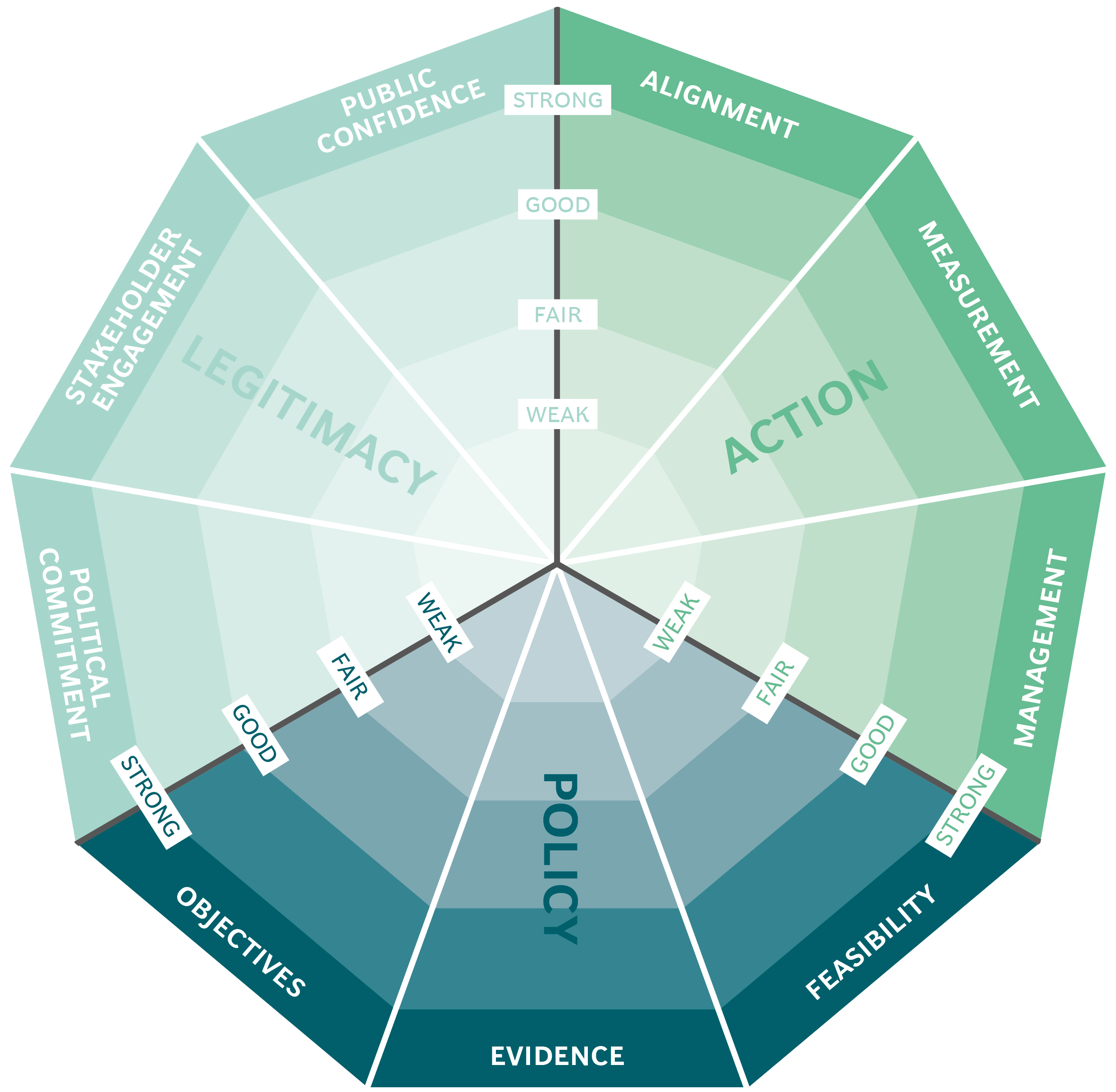

Stakeholder engagement

Researchers partnered with the Agricultural Insurance Company of India Lombard to design a suitable rainfall insurance product that insured against losses due to delayed onset of the monsoon by providing payouts at three trigger dates over two months during the monsoon season.Political commitment

There was a fair degree of support from the central government in that AICIL comes under the administrative control of the Indian finance ministry and the operational control of the agriculture ministry. There was also support from states used in the pilot, such as Andhra Pradesh and Uttar Pradesh.Clarity of objectives

The objectives of the initiative were clear and have been well maintained. Five clear options were identified that suit the varied requirements of the Indian farming community:

Strength of evidence

There was strong evidence to inform this initiative, from the extensive sample in the 63-village pilot study described above. There interesting additional findings:

Feasibility

This fiscal feasibility of this project was evaluated using the pilot study. The results from the sample study were used to evaluate feasibility and were fed into the Varsha Bima products that AICIL decided to offer.Management

AICIL kept in mind the nature and extent of the risks that it would be expected to underwrite under Varsha Bima and organising reinsurance protection from both General Insurance Corporation of India and the international reinsurers to strengthen its capacity to bear the significant risks. [2] (These risks are evident from the recent droughts throughout India.)Measurement

There have been valid indicators for measuring the success of the project:

Alignment

After the successful pilot phase, AICIL and its researchers, farmers and the Indian government were well enough aligned to make the programme successful. The Varsha Bima product is sold to farmers by BASIX, a microfinance institution, and rainfall risk is underwritten by the insurance firm ICICI Lombard and their reinsurers.

This case study has been assessed using the Public Impact Fundamentals, a simple framework and practical tool to help you assess your public policies and ensure the three fundamentals - Legitimacy, Policy and Action are embedded in them.

Learn more about the Fundamentals and how you can use them to access your own policies and initiatives.