Case Study

The Brazilian Progestão, a national agreement for managing freshwater resources

25th February, 2016

The initiative

In 2010, The Disaster Risk Financing and Insurance (DRFI) programme was set up as a joint initiative of the World Bank Group's Finance and Markets Global Practice and the Global Facility for Disaster Reduction and Recovery (GFDRR). Broadly the DRFI can be defined as “the tools and strategies to increase financial resilience against natural disasters.”

The purpose of the DRFI programme (DRFIP) was to help countries ensure that their populations were financially protected in the event of these natural disasters. It aimed to achieve this by:

The DRFI additionally promotes the development of the catastrophic risk insurance market in the private sector to offset the financial burden that would otherwise be entirely borne by the government.

The challenge

The number and scale of natural disasters appear to be on the rise, fuelled by climate change and often more extreme in their effects due to urban overcrowding. Weather conditions are becoming more extreme in many parts of the world, and the result is a catastrophic list of cyclones, earthquakes, typhoons and tsunamis.

The financial losses caused by natural disasters continue to rise, and developing countries experience the greatest impact. Such disasters generate significant risk and budget volatility. Even countries with robust disaster risk management programmes can still be badly exposed to the economic shocks caused by major disasters. A means of mitigating these risks was badly needed.

The public impact

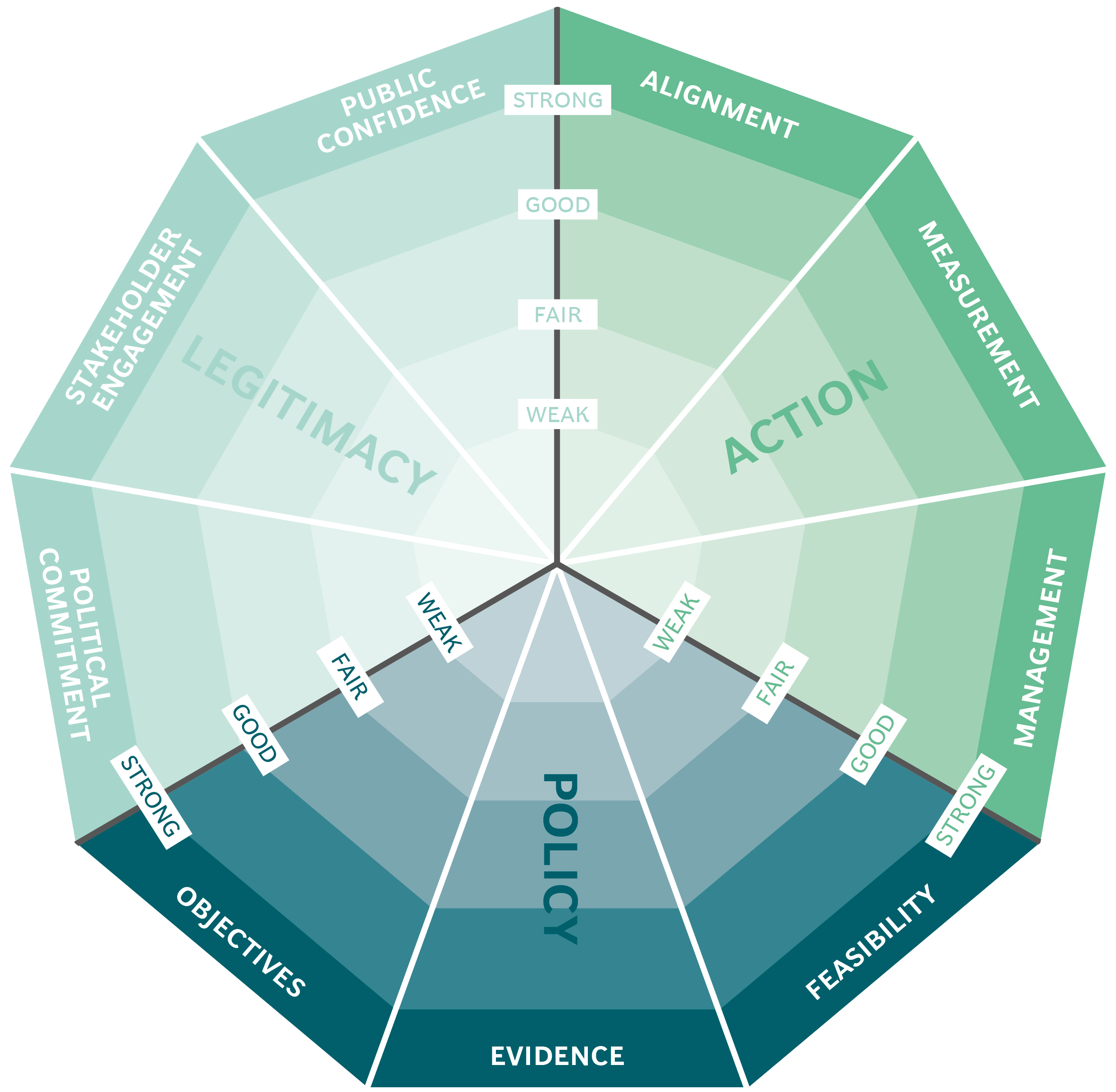

As of 2015, the DRFIP had leveraged US$3.4 billion to deliver risk financing solutions to vulnerable countries, with over US$800 million more in the pipeline. However, not all the attempts to strengthen DRFI have resulted in the operational success of its programmes, so its public impact in the first five years of life has been relatively mixed.Stakeholder engagement

There are mechanisms to involve all stakeholders - the World Bank, the GFDRR, and the DRFI member states - in the delivery of the programme, although these have not always been successful. The DRFIP required the creation of a recovery framework that was acceptable to all stakeholders. For example, the Pacific DRFIP had initial high-level government involvement, specifically from all the finance ministries and national disaster management offices in the region.

However, it suffered a setback in 2014 when the “Solomon Islands decided to withdraw from the facility as the country suffered two disaster events that did not trigger pay-outs”. [2] (One of the disasters was 2013 Santa Cruz earthquake, which “did not result in a payout because the level of physical damage caused by this event was relatively low”.) This suggested that some of the terms of the DRFI agreement might not have been acceptable to all member countries. [3]

Political commitment

The DRFIP was created after positive discussions over several years with governments across the world, and these governments, and other administrations, have shown a strong commitment to DRFI.

This commitment is confirmed whenever the positive response from electorates on receipt of post-disaster financing aid. According to a 2015 report by La Fondation pour les Études et Recherches sur le Développement International (Ferdi): “voters punish politicians for the occurrence of natural disasters in the run-up to elections ... But politicians can partially offset these effects, and sometimes even gain voteshare, by providing reconstruction funding.” [4] When such funding is not forthcoming, as with the Solomon Islands, the politicians' commitment may be withdrawn.

Public confidence

DFRI's post-disaster funding tends to result in a positive response from the public. For example, a case study showed that voters rewarded the incumbent presidential party in Mexico for delivering DRFI drought relief compensation (through the FONDEN Natural Disaster Fund in Mexico). [5] Such an analysis implies that any attempt to aid post-disaster financing will be viewed positively. (There is the potentially adverse consequence that it could influence governments to request DRFI funds more actively whenever elections were imminent.)Clarity of objectives

The DRFIP’s policy has remained consistent since its inception in 2010, but its objectives are only qualitative and its evaluation mechanism does not directly address the impact of funding on the people affected and impoverished by natural disasters.Strength of evidence

The World Bank conducted a number of studies evaluating the need for such an organisation and the impact it would have, using detailed statistical models, before setting up the DFRI. It was only created after several years of analysis by the World Bank along with other stakeholders.Feasibility

The DRFI programme was set up to improve countries' financial resilience to natural disasters. However, several countries lack the capacity and know-how to utilize the programme fully, and the approaches adopted by DRFI could be more cost-effective. In response to this, the programme is developing a framework to provide better evidence and evaluate cost-effective approaches that will enable national governments and international donors to be smarter in their support and maximise their impact.

Nonetheless, countries often lack the capacity, resources, and experience to use DRFI's existing products effectively. The technical risk information, with its vocabulary drawn from risk insurance (e.g., simulated losses, average annual losses, and probable maximum losses) is often difficult for generalist policymakers to understand. The appropriate risk modelling tools and risk data that are essential to DRFI are still absent from those countries that most need them.

Management

DRFI is a World Bank initiative and accordingly well managed and structured. The program is divided into three main service lines, Technical Assistance and Operations; Policy Advising, Knowledge Management, and Capacity Building; and Product Development. Furthermore, the DRFIP consistently produces management reports aimed at evaluating and improving the impact of the programme.Measurement

The DRFIP’s evaluation procedure fails to account for DRFI’s quantitative impact. There are very few evaluations of sovereign DRFIPs. Those that exist are inconsistent in their methodologies and typically do not directly address its specific impact on low-income groups. However, the programme is currently developing and testing a quantitative impact appraisal framework for sovereign programmes.Alignment

DRFI works with the relevant national disaster management organisations to implement the recovery programme. However, there exists a gap between the financial products DRFI offers and the ability of the countries receiving the DRFI's services to adopt them:

Bibliography

Discipline and disasters: The political economy of Mexico's Sovereign Disaster Risk Financing Program, 2015, LAURA BOUDREAU, (Chapter 12 of the above report)

This case study has been assessed using the Public Impact Fundamentals, a simple framework and practical tool to help you assess your public policies and ensure the three fundamentals - Legitimacy, Policy and Action are embedded in them.

Learn more about the Fundamentals and how you can use them to access your own policies and initiatives.