Case Study

ChileAtiende – a multi-channel one-stop shop for public services

26th February, 2016

The initiative

The VA home loan guaranty programme was originally conceived in 1944 to put the veteran on a par with his or her non-veteran counterpart. Its overall objectives “were to diminish to the greatest possible extent the economic and sociological problems of postwar readjustments of millions of men and women then serving in the Armed Forces." [2]

In 1944, as the war began to draw to a close, the government of Franklin Delano Roosevelt signed off legislation to help veterans. “The programme was one of the major innovations and a most important part of the original Servicemen's Readjustment Act of 1944, Public Law 78-346. The first legal framework was set out in Title III of that Act." [3] It was also known as “the GI Bill of Rights” or just the GI Bill.

It gave assistance to eligible veterans, active duty personnel, surviving spouses, and members of the Reserves and the National Guard in buying, retaining and adapting their homes.

The challenge

After the First World War, discharged veterans “received minimal benefits from the government. Those who were not disabled in combat received, as the Veteran's Administration today describes it, ‘little more than a $60 allowance and a train ticket home'". [1] Many found it difficult to adjust to civilian life as is shown by the 1931 film, ‘The Last Flight'.

Those who returned to the US found it difficult to make a living, especially during the Great Depression. ‘The Bonus Army', a group of veterans marched on Washington, DC in the summer of 1932 to demand full payment of their bonuses. The federal government recognised that they needed to create a more supportive policy for veterans of the Second World War, so that they would be better able to reintegrate into civilian life.

The public impact

The VA home loan guaranty programme has given assistance to veterans from 1944 to the present day:

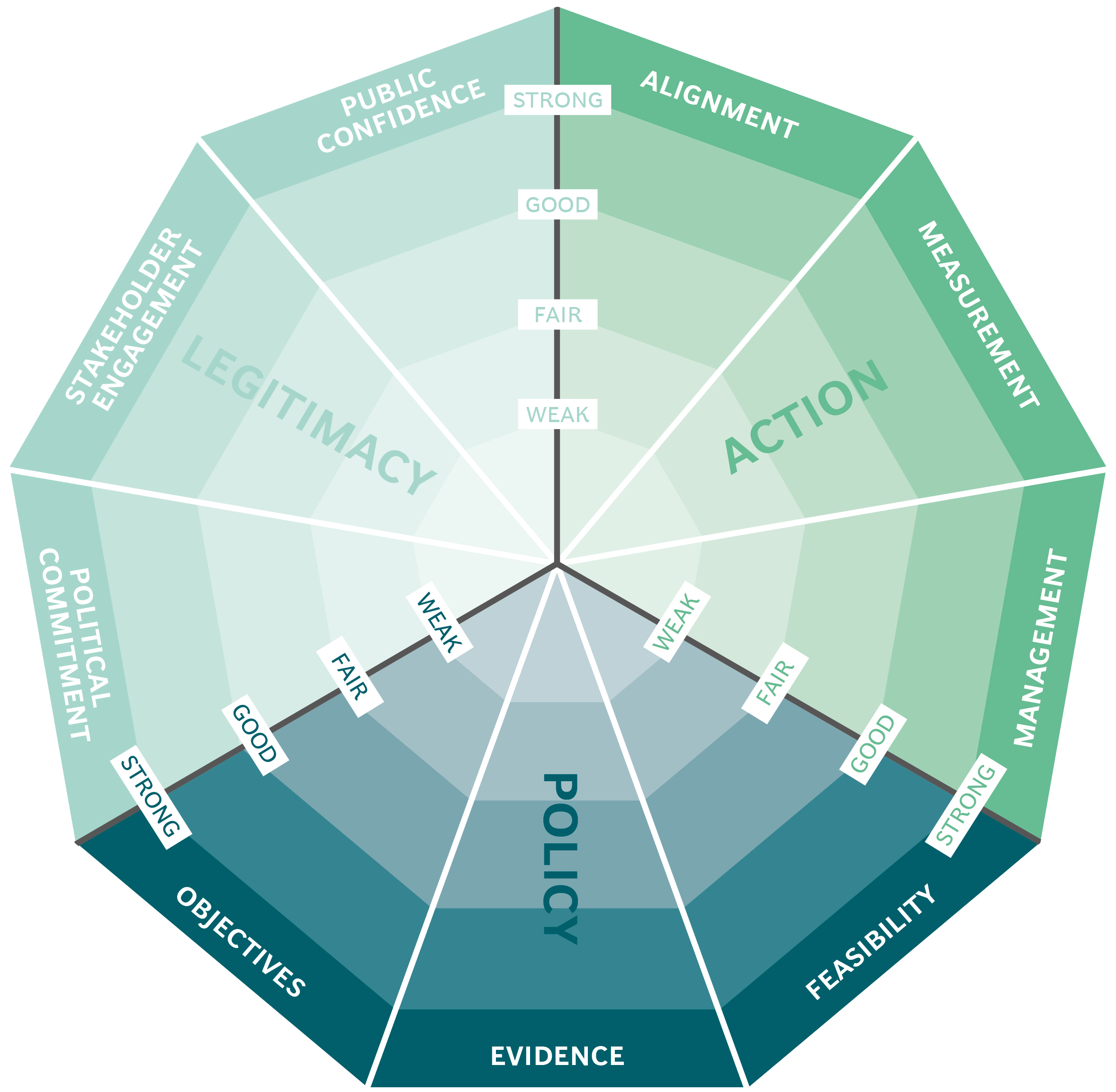

Stakeholder engagement

The idea for a veterans' home loan guaranty was initially planned and proposed by the American Legion. It found support in the Senate and was passed into law by the Roosevelt government.

The War Manpower Commission was given the responsibility of allocating funds and make available sufficient funds to carry out the provisions of the initiative. Also, to gain public support the American Legion carried out a national publicity campaign.

Political commitment

On 24 March 1944, the Senate passed the GI Bill unanimously. When signing off the legislation, President Roosevelt stated that the money spent on the initiative as "the best money that can be spent for the future welfare of the Nation." [5]

The view that veterans merited and needed this level of support was continued for veterans of the Korean War of 1950-53. “Congress readily recognised that these veterans were also entitled to aid in readjustment to civilian status upon leaving the service, and passed the Korean GI Bill, Public Law 82-550, in 1952." [6]

Public confidence

The re-election of President Roosevelt in November 1944 with 53% of the vote indicated the confidence of the public in his Democrat government.

The veterans themselves considered that the government was providing adequate support. “In 1946, Gallup asked a sample of veterans if the government had given them, as veterans, all the help they thought it should. Strong majorities of those who saw combat in WWI (75%) and WWII (69%) said that it had." [7] Many of the general public thought that they deserved more: a poll conducted in 1947 indicated that “about a third of the public in 1947 thought benefits were not adequate." [8]

This indicates that the public believed strongly that veterans should be well rewarded for their service and that some felt that not enough had been done.

Clarity of objectives

The overriding objective was clearly stated: to help veterans readjust to civilian life after the war. The specific objective was to provide credit to veterans in buying and maintaining their homes. This has been maintained since and is demonstrated by the number of veterans assisted with home loans.Strength of evidence

A number of studies of the various proposals were carried out by the Senate Committee on Finance and the House Committee on World War Veterans' Legislation. The Committee referred to “the many plans advocated and studied by the Committee." [9] The consensus was that “considering length and character of service, together with comparable sacrifices, the plan which would guarantee the most nearly uniform consideration would be an adjusted service pay”. However, the cost of such a bonus was considered to be too expensive and the alternative of valuable benefits was considered to be preferable (see Feasibility below).

The programme was formulated in the light of the unsatisfactory treatment of veterans after the First World War and was also influenced by the desire “to avoid the economic recession historically associated with postwar periods." [10]

Feasibility

The prospective costs of the legislation were considered by the Committee on World War Veterans' Legislation in 1944. “The Committee on World War Veterans' Legislation, in reporting to the House, also expressed the belief that, at this time, the proposed benefits were preferable to adjusted compensation." [11] The home loan guaranty programme was considered to be one of the financially feasible benefits. “In a way, the loan guaranty programme was advanced as an alternative device to a cash bonus, because it would be vastly less expensive to the Government, and because it would better serve the needs of veterans." [12]Management

The programme is managed by the US Department of Veterans Affairs. [13] The VA underwrites loans from private lenders (banks, savings and loans or mortgage companies) ensuring the lenders are protected if the veteran fails to repay the loan. This also eliminates the need for the veteran to pay a deposit.

The US Department of Veteran Affairs is government department with a clear management structure. It is headed by the Secretary of Veteran Affairs, who is a member of the President's Cabinet, and supported by a Chief Operating Officer and Chief of Staff. [14]

Measurement

National surveys conducted by the US Department of Veterans Affairs served as the major measurement yardstick of this programme. The “VA Loan Survey data ... describes the population of programme participants, including their demographic profile, health status, and military status." [15] This data is detailed and enables a number of metrics, such as the number of amount of loans and the average number of such loans taken out by individual veterans.Alignment

Successive governments have maintained and updated GI Bill legislation, e.g., in 1952 and 2008. The Supplemental Appropriations Act of 2008 gave veterans with active duty service on, or after, 11 September 2001, enhanced educational benefits and the ability to transfer unused benefits to spouses or children.

The veterans themselves have been, in general, supportive of the programme as part of the wider context of veterans' assistance. In 2011, Pew Research asked veterans if the government had given them all the help they thought it should and 61 percent said ‘Yes' (see also Public confidence above).

Equally, the public have been supportive of veterans' benefits. "Strong support for veterans and a willingness to provide them with any needed assistance has become, in the years since the draft was ended, a central tenet of American values. Strong majorities support a variety of government measures to improve the lives of veterans, and almost no one thinks spending on vets should be decreased." [16]

This case study has been assessed using the Public Impact Fundamentals, a simple framework and practical tool to help you assess your public policies and ensure the three fundamentals - Legitimacy, Policy and Action are embedded in them.

Learn more about the Fundamentals and how you can use them to access your own policies and initiatives.