Case Study

Mexico City's ProAire programme

26th February, 2016

The initiative

The ACA took effect in 2010 and had as its two main goals providing better health insurance coverage for Americans and lowering the overall cost of healthcare. The programme aimed to extend health insurance to some of the estimated 16% of the population without access - covered neither by their employers nor by national programmes for the poor and elderly.[3]

The ACA changed the regulation of health insurance essentially in five ways, the first of which was extending federal regulation to most private insurance companies, which historically in the US had been regulated at the state level. The ACA specified some requirements of insurers, most significantly that private insurers must sell (or issue) a policy to any person who wants to buy one, regardless of their health status or risks. The federal government also offers financial assistance to states to improve their ability to review insurance premium rates and enforce compliance with the law.

The second reform establishes a "minimum coverage", requiring all citizens and lawful residents to obtain health insurance coverage or pay a penalty (this removes the incentive for only getting insurance when people become ill, thus addressing the risk for private providers). There are exceptions for very low-income people who could not afford this, as well as individuals who do not believe in medical care for religious reasons.

The third reform is the requirement for the establishment of health insurance exchanges as a marketplace where individuals and small businesses can buy insurance (people are also free to buy directly from an insurance company). The federal government will provide subsidies to individuals with incomes between 100% and 400% of the Federal Poverty Level to enable them to pay for the premiums. Most exchanges are run by the states, and the federal government has the authority to operate a federal exchange in states that fail to create their own. States also have authority to add further requirements to their health plans, meaning that plans may differ across states, especially in price.

The fourth reform encourages private employers to provide health insurance to employees - although it does not oblige them to. Finally, the fifth reform addresses the remaining people who cannot afford to buy insurance, primarily because they are not eligible for federal subsidies - both individuals and small businesses. For this group, the ACA amends the Medicaid statute to make everyone with an income below 138% of the Federal Poverty Level eligible for Medicaid health benefits, and the federal government will pay for 100% of the cost of adding this group to Medicaid, ultimately paying 90% by 2016. However, the US Supreme Court held that the states are not obliged to comply with this eligibility standard, so people living in states that decide not to comply may be left without coverage.[4]

The challenge

In 2008, the US healthcare system was historically considered to be lagging behind its global peers in terms of efficiency and coverage. Two of its key characteristics pointed to a need for reform: "It spends far more per person on healthcare than any other country, yet it is the only country in the developed world that fails to provide healthcare coverage for almost all of its residents".[1]

One of the reasons that made the American system so expensive was that over half of the population relied on private insurance - mostly sponsored by employers. Otherwise, the federal Medicare programme only covered people with disabilities or retired people aged over 65 years. Medicaid - a joint state and federal programme - covered people with low incomes, but in most states it was limited to those fitting certain categories, such as single parents, children, and pregnant women. People who did not fit into any of these categories found it hard to obtain individual insurance. This was not only because of its cost but also that people were subject to very thorough screening (medical underwriting), which usually either declined people with existing medical conditions or charged them substantially more without even covering them for their existing ailments.

Figures from 2010 indicate that approximately 50 million people (16% of the population) had no public or private health insurance coverage, while national spending on medical care in the US at the time was close to USD3 trillion a year.[2]

The public impact

The ACA has managed to extend coverage to a certain extent, but it has also been adversely affected by increases in premiums and by the public controversy occasioned by political issues and mismanaged expectations:

Stakeholder engagement

There were numerous stakeholders involved in the formulation of Obamacare, including the following: federal and state governments, health insurers and other commercial groups related to the policy, political parties and leaders, National Republican Congressional Committee, the Supreme Court, and the general public.

This was reflected in a wide spectrum of opinions regarding what the legislation should look like. The debate between Democrats and Republicans indicates their contrasting positions: "Democrats in the US were in favour of a more socialised solution for healthcare reform, that is, to expand Medicare or create something like it that, along with Medicaid, covered everyone in a 'single payer' system, like that in Canada. While Republican proponents supported a 'less ambitious' law that uses government subsidies mainly to help only those people who are not insurable, leaving the rest of the market to function as normal."[10]

The administration has claimed to have learnt from previous experiences to obtain stronger support for this policy: giving Congress more input to the structure and more information about the policy goals, as well as looking to get support from industry specialists, including insurers, physicians, pharmaceutical companies, hospitals and other providers, and allowing the House and Senate to work through each of their concerns before merging these into a bill.[11]

Political commitment

Previous healthcare programmes in the US had received more consensual support from political leaders, while the ACA occasioned much more dispute. It was favoured by Democrats but strongly opposed by Republicans.

The process for approval of the ACA bill was also conflictual: “Republicans in the House have voted to delay, 'defund' or repeal the law some 60 times”[12] and it barely made it through Congress in 2010, with a slim Democratic majority. Amid extreme partisan divides along ideological lines, it faced all-out Republican opposition. In March 2010, the ACA was only narrowly passed by the House (by 219 votes to 212), with all 178 House Republicans voting against. "These numbers underline the exacerbated partisanship in Congress and, more generally, the lack of consensus surrounding this reform.”[13]

Public confidence

Obamacare has been widely debated both among political actors and the general public. Given that its measures have affected people differently (for better and worse), support and approval have been mixed and changing since implementation, and the public seem to be split down the middle in terms of overall support.

According to a Pew Research Center survey from February 2015, a greater share of the public disapproves (53%) than approves (45%) of the ACA.[14] A Kaiser poll found similar results in 2015, with 43% holding a favourable view as against 42% with an unfavourable one. These figures, however, represented an improvement for Obamacare on a previous survey in July 2014, which found only 37% of Americans supporting the policy, compared to 53% who rejected it.[15]

Clarity of objectives

The main goals of the ACA were to provide more Americans with health insurance and lower the overall cost of healthcare. When launching the ACA, President Obama gave some measurable estimates that helped reinforce these general objectives:

Strength of evidence

Evidence used for the implementation of Obamacare was based principally on the existing healthcare system in Massachusetts while there was also input from the testing of pilot programmes aimed at improving the quality of service to users.

Obama declared that the ACA was modelled on Mitt Romney's healthcare initiative in Massachusetts. “It's because you guys had a proven model that we built the Affordable Care Act on this template of proven bipartisan success. Your law was the model for the nation's law.”[18] The Romney plan itself has received mixed support, with significant praise of its model from some fellow Republicans, but also some criticism about its method. "The healthcare plans advocated by all three of the leading Democratic presidential candidates — Hillary Clinton, John Edwards, and Barack Obama — are all substantially the same as Romney's. They are all variations of a concept called 'managed competition', which leaves insurance privately owned but forces it to operate in an artificial and highly regulated marketplace similar to a public utility."[19]

Opinion on the Massachusetts model is divided, with some taking the view that it was ineffective. "As Massachusetts has shown us, mandating insurance, restricting individual choice, expanding subsidies, and increasing government control isn't going to solve those problems. A mandate imposes a substantial cost in terms of individual choice but is almost certainly unenforceable and will not achieve its goal of universal coverage. Subsidies may increase coverage, but will almost always cost more than projected and will impose substantial costs on taxpayers. Increased regulations will drive up costs and limit consumer choice."[20]

Additionally, the ACA has added a number of new and amended and/or extended demonstration and pilot programmes. For example, it created the Centers for Medicare and Medicaid Innovation (CMMI), tasked with developing and funding demonstration projects to improve the quality of care for patients.[21]

Feasibility

Policymakers considered the financial and legal constraints before formulating the ACA, but might not have assessed such constraints to their fullest extent. The federal system in the US allows states to have autonomy in the application of certain legislation, which was the case for this healthcare reform. "The Supreme Court's 2012 ruling found the ACA constitutional, but also struck down a provision saying states had to change how they administered the government health programme, Medicaid. Under Obamacare, states were supposed to expand the number of people who qualified for Medicaid, which had been reserved for the poor, and in return the federal government would provide the states more funding. The court said states could choose not to participate in Medicaid expansion.”[22] This was the case for some states which decided to opt out of the Medicaid expansion, leaving people who were supposed to get coverage outside the bill's auspices.[23]

Overall, the Medicaid expansion proved to be more expensive than was forecast. "Total federal spending on the expansion in 2015 was at least 50% above Congressional Budget Office's (CBO) 2014 projection of USD42 billion. Part of the reason for this unanticipated expense is that states are paying insurers higher rates than the government projected; in fact, spending per newly eligible enrollee was 49% higher in 2015 than was expected by the Obama administration in a 2014 report.”[24]

As a result of the ACA, premiums were predicted to rise by 25% in 2017, and government subsidies were to increase accordingly to help pay for insurance. However, those who should be covered by the Medicaid expansion were ineligible for those subsidies, and some may therefore be unable to afford health insurance at all.[25]

Management

The Department of Health and Human Services (HHS) was responsible for implementation of the ACA, and faced substantial challenges. The diversity of the country - both in terms of individuals as well as the federal system - makes this programme difficult to implement. Accounting for the rights of all 314 million individuals made the management of the programme very difficult.

There are many examples of exceptions from the requirements of the ACA, of which the following is one. "An example is the contraception insurance requirement in health plans without 'cost-sharing' under the law's market reforms. This posed a serious issue for religious companies. The Department of Treasury, Labor and Health and Human Services recently provided an exception for non-profit religious employers. Unfortunately, this exception does not extend to for-profit employers. This is one example of how an exception was required."[26] It is expected that many similar exceptions will be requested in the future.

Measurement

The performance of the policy has been evaluated based on a number of indicators such as the number of people insured, the rise or fall in insurance premiums, and the number of enrolments in the policy. The main institution in charge of tracking indicators is the CBO, but, given the high profile of the policy, there are also several independent institutions and research firms tracking results and opinion, such as the Cato Institute and the Kaiser Foundation.

The CBO analyses the effects of the ACA under current law, and the effects of proposals to change the law. It regularly publishes a range of reports addressing costs, estimates and outlook related to the ACA.[27] For example, its report on "Federal Subsidies for Health Insurance Coverage for people under age 65: 2016 to 2026" was published in March 2016 and contained a number of projections of the ACA's impact. “CBO and JCT [the Joint Committee on Taxation] updated their estimates of the number of people under age 65 who have health insurance from various sources as well as their projections of the federal subsidies associated with that coverage. Those projections encompass a broad set of budgetary effects that operate under current law, including the effects of providing preferential tax treatment for employment-based coverage, costs for providing Medicaid coverage to people under age 65, and payments stemming directly from the ACA.”[28]

Alignment

The bipartisanship affecting this policy had a significant influence on the collaboration and alignment between the actors involved in its implementation. There were some states that did not approve of the policy, which resulted in a fragmentation of its execution across the nation. The lack of support from certain states continues to exert a direct impact on the coverage of the policy, as they have the right to refuse the extension of Medicaid coverage. “Even if Republicans and conservatives continue to mount fierce political attacks calling for the repeal or gutting of the entire law, more consequential obstruction comes from state-level governors and legislators who can refuse to help establish exchanges to market subsidised private insurance and, more importantly, can block outright the expansion of Medicaid.”[29]

The interdependency of factors has repercussions across the board, affecting the costs and incentives affecting other actors, including the private sector. “Insurance companies are backing out of participating in Obamacare because fewer Americans than anticipated are signing up; that in turn raises insurances costs for everyone, which then further drives down participation. For some middle-income Americans, the subsidies available for buying Obamacare policies are not generous enough, and the fines for not having coverage are too small to encourage them to enrol in plans.”[30]

Bibliography

7 Obamacare failures that have hurt Americans, Diana Furchtgott-Roth, 25 March 2016, Marketwatch

Affordable Care Act, Congressional Budget Office

Affordable Care Act Facts, Obamacarefacts.com

Lessons from the Fall of RomneyCare, Michael D. Tanner, January/February 2008, Cato Institute

MN Gov says ObamaCare “no longer affordable”, Brian Sikma, 13 October 2016, The Insurgent

Obama Says Romney's Example Shows Health Care Reform Will Work, Denver Nicks, 30 October 2013, Time

Stakeholders spend big on ACA ads, Paige Winfield Cunningham, 1 October 2013, Politico

The Politics of Obamacare, Social Security and Medicare, Scholars Strategy Network

The Real Story of Obamacare's Birth, Norm Ornstein, 6 July 2015, The Atlantic

Why is Obamacare so controversial?, 11 November 2016, BBC News

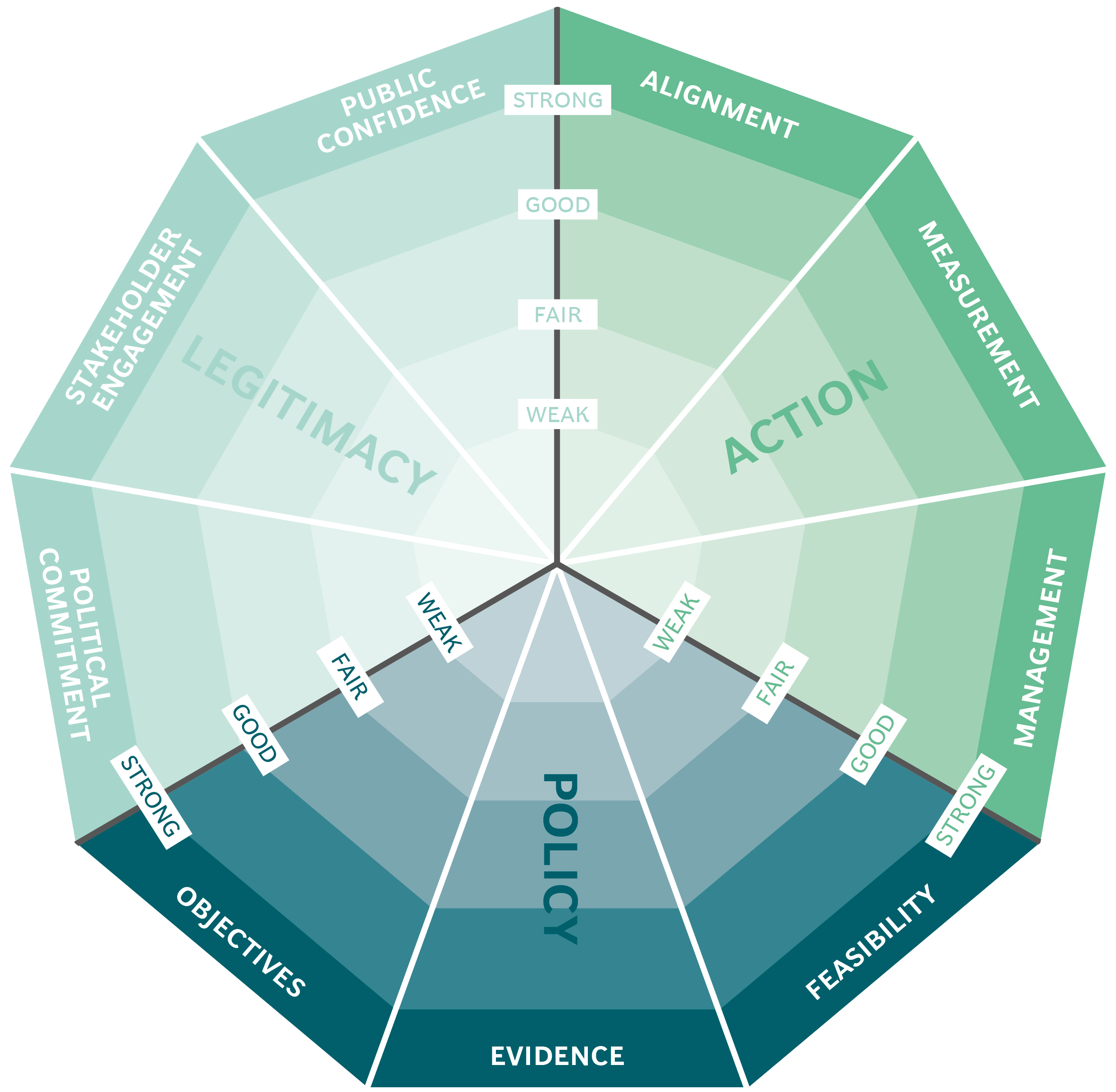

This case study has been assessed using the Public Impact Fundamentals, a simple framework and practical tool to help you assess your public policies and ensure the three fundamentals - Legitimacy, Policy and Action are embedded in them.

Learn more about the Fundamentals and how you can use them to access your own policies and initiatives.