Case Study

ChileAtiende – a multi-channel one-stop shop for public services

26th February, 2016

The initiative

The Postal Savings Depository Act of 1910 was passed by Congress on 25 June, 1910 and became effective on 1 January of the following year, establishing the postal savings system in the US. Under the system either “certificates or savings stamps could be issued to depositors as proof of their deposit and could be exchanged in amounts of US$20 or more for postal savings bonds, which yielded 2% interest rate on accounts under US$500." [1]

It was modelled on the British post office savings system. “Charles William Sikes, a member of a prominent Huddersfield banking family ... presented a measure for a Post Office Savings Bank that found favour with both Rowland Hill [the secretary to the Post Office] and the chancellor of the exchequer, William Ewart Gladstone, who successfully steered a bill through Parliament despite strong opposition from the City and the Bank of England. It received the Royal Assent on 17 May 1861 and the first such bank opened on 16 September 1861." [2]

In 1871, US Postmaster John Creswell recommended that the federal government emulate the British postal savings system. The idea was discussed by successive administrations, but the financial crisis of 1907, and the subsequent runs on private banks, gave it the necessary impetus. President Theodore Roosevelt responded by advocating a post office savings system to meet the needs of small savers and local communities and it passed into law during the administration of his successor, William Howard Taft.

The challenge

In the 19th and early 20th centuries, the majority of Americans had no secure and convenient place to keep their money. Many were unwilling to entrust their savings to a private bank, which was always at risk of failure. This was thought to mean that American workers would be less likely to save their money than if there were an accessible and secure place to invest it, and which was backed by the government.The public impact

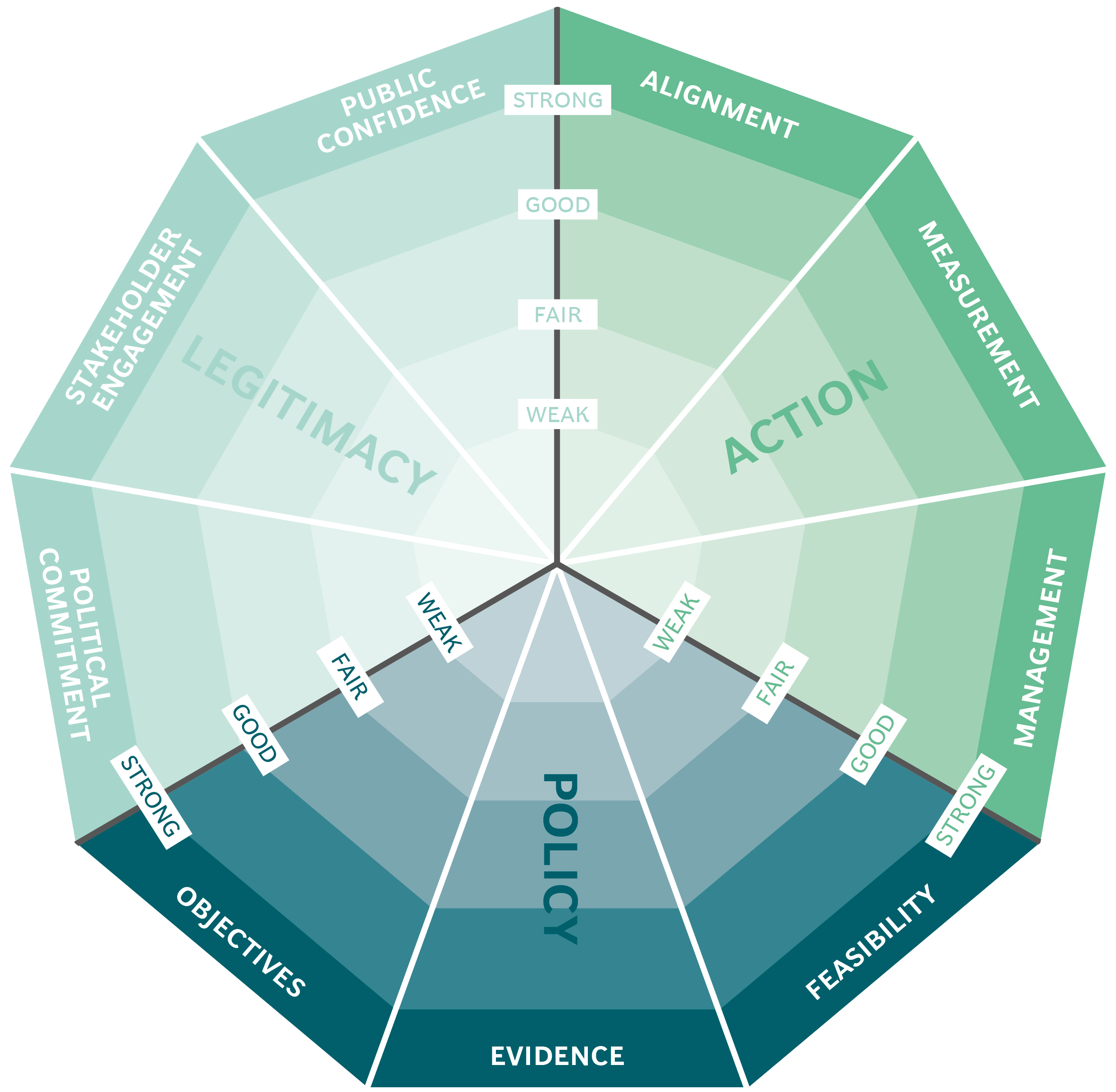

The system hit its peak “in 1947 at almost US$3.4 billion, with more than four million depositors using 8,141 postal units." [3] By 1964, however, it had achieved its goal and new directions in investment meant that the amount held in postal savings had declined to US$416 million. This led to the programme being discontinued in 1966-67.Stakeholder engagement

The main stakeholders were President Taft, the board of trustees (which included senior government members), the postmaster general in the Taft administration, Frank A. Hitchcock of Massachusetts, Congress, and the investors in postal savings. Banking reform became a major issue in the 1908 presidential elections, as a result of the banking crisis, and President Taft had campaigned for postal banking as a means of stabilising the nervous banking sector and helping credit-starved regions such as the American South and West.Political commitment

President Taft was firmly committed to postal banking, as is evident from his inclusion of the subject in his campaign. His support was not in itself sufficient to overcome completely the opposition of the banks and the Democrat Party. “The Postal Savings Bank Bill, as passed, finally acquiesced to both localism and private bankers by mandating that almost all of the postal deposits stay in the community of origin." [4]Public confidence

President Taft campaigned on postal banking and won the election. He defeated his Democrat opponent, William Jennings Bryan, by 321 electoral votes to 162. This demonstrates that the public had trust in his candidacy and, by implication, to some extent in his campaign policies.Clarity of objectives

The main objective of instituting a postal savings system was to provide the entire American people with a secure and convenient means of saving their money. It was also hoped that it would free up hoarded money that was kept in less accessible regions of the country in people’s own homes.Strength of evidence

The British post office savings system had been in operation for almost 50 years at the time that the American bill was proposed. It provided clear evidence that a government-backed initiative would encourage an influx of money from small savers. The 1907 financial crisis, with its disastrous effect on personal savings in many private banks, provided evidence that the existing system was inadequate.Feasibility

The 1910 Act gave statutory force to the postal savings initiative. It was also financially secure: in order to run the operation, the postal savings system retained 0.5% of the interest paid on savers' deposits. The amount of interest paid on money on deposit was 2%, which was sufficient to persuade the public to open postal savings accounts.

The Post Office Department implemented the system in phases with a trial period at 46 depositories, opening one in each state and territory on 3 January, 1911.

Management

The postal savings system was operated by the US Post Office Department. The administration of the system was headed by a senior and experienced board of trustees. Moreover, the US Postal Service has a very clear organisational structure, with board of governors, the postmaster general and its executive team, and the postal leadership. The board of trustees consisted of the postmaster general, the secretary of the treasury and the attorney general.Alignment

The alignment of the stakeholders was in question from the initial proposal of a postal savings system, by the postmaster general, John Creswell in 1871. The bankers and the Democrats were unenthusiastic and opposed the idea. They claimed, for example, that anyone with money to save was already saving it or objected to the idea that the deposits would go directly to the Treasury. It was only through the combination of circumstances – of President Taft’s enthusiasm (and President Roosevelt’s before him) and the financial crisis – that gave the idea sufficient traction to be realised.

This case study has been assessed using the Public Impact Fundamentals, a simple framework and practical tool to help you assess your public policies and ensure the three fundamentals - Legitimacy, Policy and Action are embedded in them.

Learn more about the Fundamentals and how you can use them to access your own policies and initiatives.