In 2005, the Philippines government needed to give its citizens easier access to credit. So it developed the Microfinance Development Programme (MDP), with a focus on raising the incomes of the poor.

[1]

The initiative

The government responded with a programme of reforms - the MDP. It formed an important part of their overarching poverty reduction objectives and had three key components:

- Enhancing the enabling and regulatory environment of microfinance. This was intended to promote market efficiencies and outreach of services at competitive prices.

- Building viable microfinance institutions (MFIs) that could provide efficient and cost-effective retail delivery of services to the poor.

- Increasing financial literacy and consumer protection for the users of microfinance services.

The MDP was included in the Country Strategy Programme 2005-07, and implementation began in December 2005.

The challenge

The Philippines government saw a pressing need to increase household incomes and address the poverty and vulnerability of many of its people. But citizens had limited access to credit instruments such as housing loans, agri-loans and micro-insurance. How could the government address the systemic weaknesses in the microfinance sector and make it thrive?

The public impact

The MDP came to an end in December 2007, by which time:

- Outreach had increased from 1.3 million active borrowers in 2004 to 2.1 million by 2008. However, many of the poor were refused credit because they didn't have the capacity to repay a loan (a Catch-22 situation).

- There were positive rates of return on assets and equity. The MFIs demonstrated sustainable operations, with increases in financial education and consumer protection.

- The increase in loans to micro-enterprises and the new jobs created did result in some increase in household incomes. But the programme's relevance and effectiveness diminished because of its slow implementation.

In summary, the government had achieved a relatively sustainable and diverse, market-oriented microfinance sector with a wide outreach at competitive prices. However, it needed to speed up structural reforms and encourage MFIs to lend to poorer citizens.

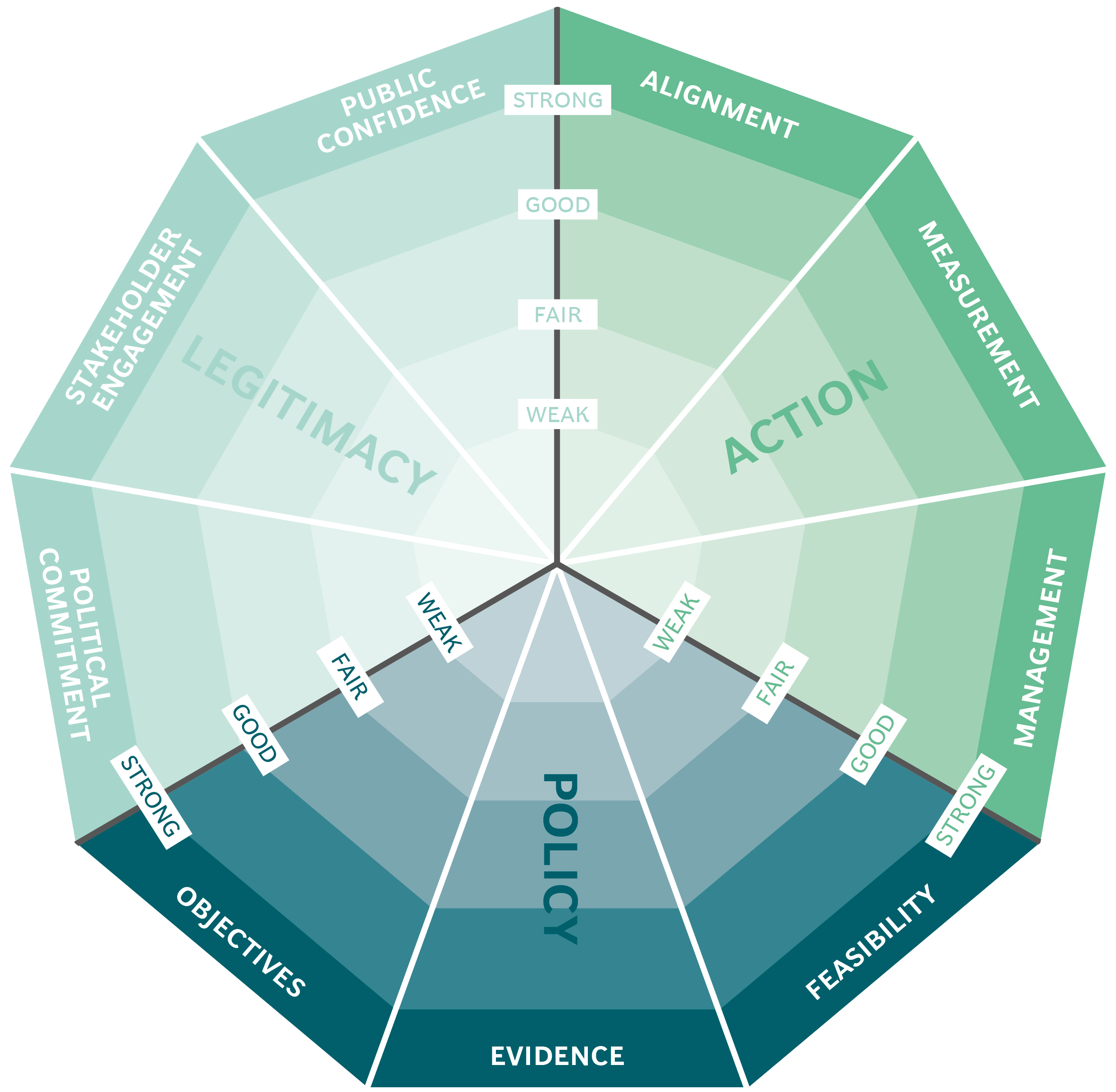

Stakeholder engagement

The stakeholders were involved in all the stages of the MDP, and their participation formed one of its core conditions:

- The government collaborated with the banking community, cooperatives, NGOs, and the aid community in promoting microfinance as a poverty reduction tool and in achieving greater outreach and sustainability.

- The key factors that contributed to the success of the MDP included “the strong commitment of the government and support from stakeholders to develop the sector and achieve sustainable microfinance.

- The Asian Development Bank (ADB) provided significant loan capital and was a major stakeholder. This enabled the Philippines government to address systemic weaknesses in the microfinance sector.

Political commitment

This was a government initiative and, as a result, the project received strong political commitment:

- The MDP was a part of the government's Country Strategy Programme 2005-07 and was therefore closely aligned with its overall priorities.

- There was clear commitment from the government for the development of the microfinance sector and expansion of financial services to the poor, as embodied in the MDP.

Public confidence

Some efforts were made to consult the public, although not entirely successfully:

- Six public consultations were held, as this was a core condition of the ADB loan. However, the MDP server, envisaged as a platform for collecting public complaints, was not used.

- There were public objections to certain provisions within the MDP. This led to a careful staff assessment by the ADB and discussions with stakeholders to determine the impact of those provisions on the policy environment. They concluded that the provisions had no major negative impact on the development of the microfinance sector.

Clarity of objectives

The policy actions under the programme were all maintained and achieved:

- All the policy objectives were met. The envisaged outcome - of achieving a sustainable and diverse market-oriented microfinance sector with expanded outreach at competitive prices for the poor - was realised, although the last of these is qualified below.

- The programme design was an appropriate response to the identified sector issues and constraints - the weak supervisory capacity of the Cooperative Development Authority (CDA), weaknesses in the regulatory and supervisory framework, the limited capacity of MFIs to expand outreach, and the lack of financial literacy and consumer protection among poor and low-income households.

Strength of evidence

Microfinance in the Phillippines was based on a sound business model, patterned after Grameen Bank in Bangladesh.

[2] Microfinance has also been shown to be a “potent tool for poverty reduction.”

Feasibility

In defining the MDP, some aspects of resourcing and scheduling were given due consideration but there were weaknesses in other aspects:

- ADB fact-finding and appraisal missions were conducted to identify the sector issues and constraints and to develop and design the components for the MDP.

- The financing was given due consideration; a loan and a grant were approved early on in the MDP (a programme loan of $150 million accompanied by a technical assistance grant of $500,000 and a grant, financed by the Japan Fund for Poverty Reduction, of $900,000 for capacity development of savings and credit cooperatives and for strengthening the regulatory capacity of the CDA).

- The MDP's information system was not assessed early on and so the relevant policy actions could not be incorporated.

- While reducing poverty was one of the objectives of the programme, the extent of poverty reduction is not known. There were no explicit indicators for monitoring poverty impact, and nor was baseline data established on the income or poverty levels of microfinance clients.

Management

Overall, the programme was managed effectively:

- The performance of the National Credit Council (NCC) was rated ‘highly satisfactory' by the ADB. In their view, the NCC played a leading role in overseeing the implementation of the programme and in coordinating programme activities among implementing agencies and the ADB. The NCC was effective in coordinating the implementation of policy actions called for in the programme and was responsive to issues that arose during implementation.

- Implementation agencies delivered the expected outputs based on the MDP policy matrix.

- A consulting firm with expertise in the microfinance sector provided training on relevant aspects of the programme. The performance of the consulting firm was satisfactory, according to the ADB, as it delivered the expected output.

Measurement

While the majority of the outcomes could be measured, there was a significant lack of relevant indicators to measure poverty reduction (one of the main objectives of the project, see Policy: Feasibility above):

- Most of the outcomes had clear monitoring procedures, and reported data from these indicators was used to make further recommendations.

- The MDP had no explicit indicators for monitoring poverty impact. Nor was baseline data established on the income or poverty levels of microfinance clients. The results from the project were also used to influence further policy decisions by the government.

Alignment

There was a certain lack of alignment between the executing bodies, which diminished the relevance of the programme:

- There was slow progress in the implementation of the rationalisation plan, due to changes that needed to be made to align it with the New Cooperative Code and the bureaucratic processes involved, particularly in the review and approval of new positions.

- A Memorandum of Agreement (MOA) was signed by the government regulatory agencies, government financial institutions, and other stakeholders to adopt and implement performance standards for MFIs.