Case Study

The Brazilian Progestão, a national agreement for managing freshwater resources

25th February, 2016

The initiative

The India Infrastructure Finance Company Ltd (IIFCL) was established in January 2006 as a wholly-owned Government of India company. It began operations in April 2006 with the objectives of:

The creation of the IIFCL was intended to address regulatory and other restrictions and to raise affordable long-term funding from the financial markets to lend to PPP projects, while keeping the intermediation costs to a minimum.

To ensure that IIFCL delivered on its mandate, a detailed framework was set out to guide its project selection, lending principles, approval processes, and deployment of resources. There was a new government structure for promoting PPP, including an infrastructure committee under the chairmanship of the prime minister and a formal, streamlined mechanism for appraising and approving PPP projects.

For infrastructure projects which were economically justified but not commercially viable, the government introduced a scheme for providing capital grants of up to 40 percent of project costs.

The challenge

Until recently, India's infrastructure was beset with problems and used out-of-date technology. The roads, railways, ports, airports and power supply were inadequate and inefficient.

Before the market liberalisation of the 1990s, “infrastructure projects were typically financed from the limited resources of the public sector, which was characterised by inadequate capacity addition and poor quality of service”. [1] In the 1990s, the economy grew rapidly - by 7%-9% a year - and the pressures on infrastructure increased. As a result, infrastructure came to be regarded as a major constraint in sustaining the rapid growth and in attracting investment or doing business in India.

Initial reforms failed to stimulate enough private investment in infrastructure, as there was only about US$55 billion investment during the period of the ‘tenth five-year plan' (2002-07). Total investment was only about five percent of GDP, as compared to around ten percent in the East Asian economies. As a result, there was a growing realisation of the need to increase the flow of private capital into infrastructure in order to maintain growth, alleviate poverty, and improve the quality of life.

The public impact

In the period from April 2006 to March 2015, the IIFCL had been involved in a number of infrastructure improvements, and it had:

These initiatives spurred rapid growth in Indian infrastructure lending by banks, which increased from around US$1.4 billion in 2000 to US$173 billion in 2013. [2]

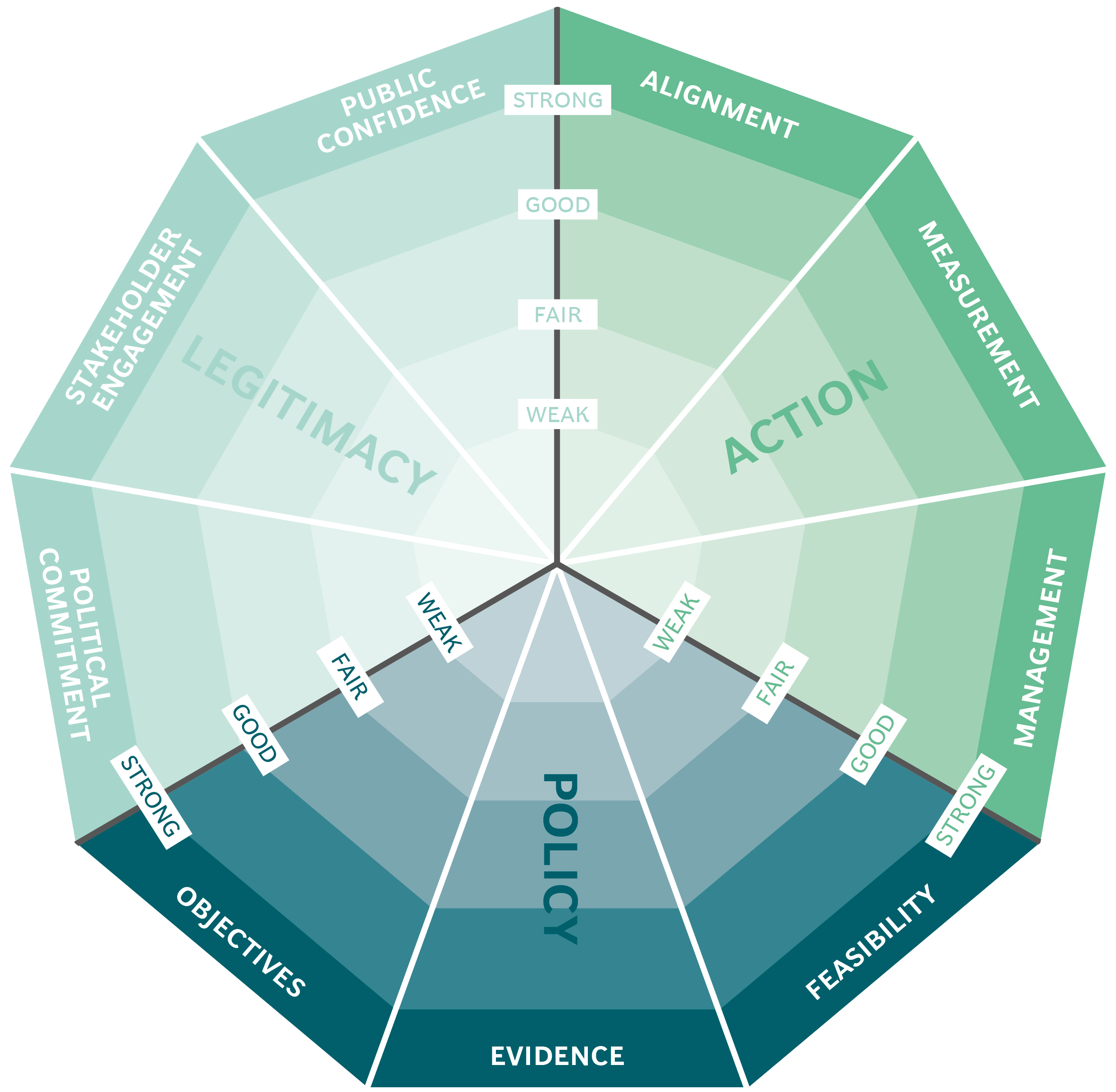

Stakeholder engagement

The major stakeholder in launching the IIFCL platform was the Indian government of India. The Ministry of Finance and the Prime Minister's Office played major role in its launch and supplied investment guarantees. Other ministries supported the initiative by streamlining and simplifying the IIFCL’s procedures. However, there was no information on the degree of engagement of external stakeholders, such as industrial bodies and business community.Political commitment

The finance minister said, while presenting the Indian Union Budget for 2005-2006, “acknowledged the need and significance of building adequate infrastructure in the country and made the following announcement [3]: ‘The importance of infrastructure for rapid development cannot be overstated. The most glaring deficit in India is the infrastructure deficit. Investment in infrastructure will continue to be funded through the Budget. However, there are many infrastructure projects that are financially viable but, in the current situation, face difficulties in raising resources. I propose that such projects may be funded through a financial Special Purpose Vehicle.'” This shows the government's priority in creating such a vehicle, which eventually took shape as the IIFCL.

The government also committed to a guarantee of INR100b (USD $1.5b) as a guarantee to IIFCL for its first year of operation, which shows that government was willing to spend capital to support its policy.

Public confidence

In 2006, opinion polls indicated that the majority of people had confidence in the government after Dr Manmohan Singh’s one year in office has been a success. [4] This period coincided with IIFLC’s planning stage and suggested that the prime minister had the support of the public at the time of the reform.Clarity of objectives

The objective stated at the outset – to increase private investment in infrastructure through PPP – was clear and formed part of the government’s policy on infrastructure investment. This objective has been maintained throughout the IIFCL’s ten-year existence: by March 2015, “the IIFCL had approved 342 projects that would mobilise private investment of USD 110 billion, of which the IIFCL’s share would be about USD 12 billion”. [5]Strength of evidence

The government well understood the need to raise investment to push the infrastructure projects that had become stalled without sufficient investment and PPP was an appropriate choice. While setting up the IIFCL, the government did not look at external models, because PPP was not a new instrument in the Indian economy. In addition, it had proved to be a successful vehicle for other major infrastructure projects in the developing world.Feasibility

It was argued that, by encouraging private sector involvement, efficiency gains could be realised because private players are more focused and can bring in economies of scale. Additionally, the cost burden on the government would reduced, as the overall cost would be spread over a much longer period.

However, there were challenges associated with debt financing. Since PPP projects are usually financed on a 30:70 ratio of equity to debt, the mobilisation of the requisite funding was a difficult task, though not infeasible.

A prominent feature of the PPP architecture was the adoption of model documents such as model concession agreements, model RFQ, model RFP and other bidding documents. These initiatives, especially the standardisation of documents and processes, helped in the rapid roll-out of PPP projects.

Management

The IIFCL is chaired by S. B. Nayar, who has nearly 40 years' experience in the finance industry, including experience in international and investment banking as well as life insurance. He was very familiar with the IIFCL's delivery context. The IIFCL raised funds in consultation with the Department of Economic Affairs, ensuring that there was good management control from other areas of government.

The IIFCL's borrowings were guaranteed by the Government of India but carefully controlled and monitored. The extent of the guarantees was set at the beginning of each fiscal year by the Ministry of Finance, within the limits available under the Fiscal Responsibility & Budget Management Act 2003.

Measurement

The measurement and monitoring of the IIFCL is carried out by the High Level Committee on Financing Infrastructure. For instance, the committee recommended that the IIFCL should “substitute its direct lending operations by guarantee operations that would enable the flow of non-bank long-term credit for infrastructure projects, especially, insurance and pension funds. [6] Moreover, instead of continuing to borrow solely on the strength of sovereign guarantees, it should start raising funds on the strength of its balance sheet”.Alignment

There was collaboration between the IIFCL and financial institutions such as the Asian Development Bank (ADB), the World Bank, the German development bank (KfW), and the European Investment Bank. The IIFCL launched its credit enhancement initiative with the support of the ADB.

Also, private sector banks lent about USD 173 billion in 2013 for infrastructure projects.

As indicated above, he IIFCL raised funds as and when required in close consultation with the Department of Economic Affairs, one of its internal stakeholders. This indicated a coordinated approach within government.

Bibliography

Setting up IIFCL, The India Infrastructure Finance Company Ltd. (IIFCL)

IIFCL to launch credit enhancement scheme, Vrishti Beniwal, 27 February 2013, Business Standard, New Delhi

UPA birthday: More credits than debts, 21 May 2005, The Tribune, Chandigarh

This case study has been assessed using the Public Impact Fundamentals, a simple framework and practical tool to help you assess your public policies and ensure the three fundamentals - Legitimacy, Policy and Action are embedded in them.

Learn more about the Fundamentals and how you can use them to access your own policies and initiatives.